SAN ANTONIO — You’ve most likely heard of cryptocurrencies like Bitcoin and non-fungible tokens (NFTs). These digital assets operate on what’s called blockchain technology.

Blockchain technology is a digital system that allows users to record, store and manage information. A simple way to think of it is like Google Docs. Multiple users can use this online tool to collaborate, edit and insert information instantaneously.

Blockchain technology is similar to Google Docs except that users cannot change information once it’s in the system. Also, this system is decentralized, and the stored information can be verified by multiple users.

“Blockchain, if you think about it, is really just a database. It’s a ledger, but it has transactions on it,” explained Karl Eggerss, senior wealth advisor and partner of Covenant. “One of the easiest examples right now is cryptocurrencies. When they’re bought and sold, it’s being recorded in this ledger.”

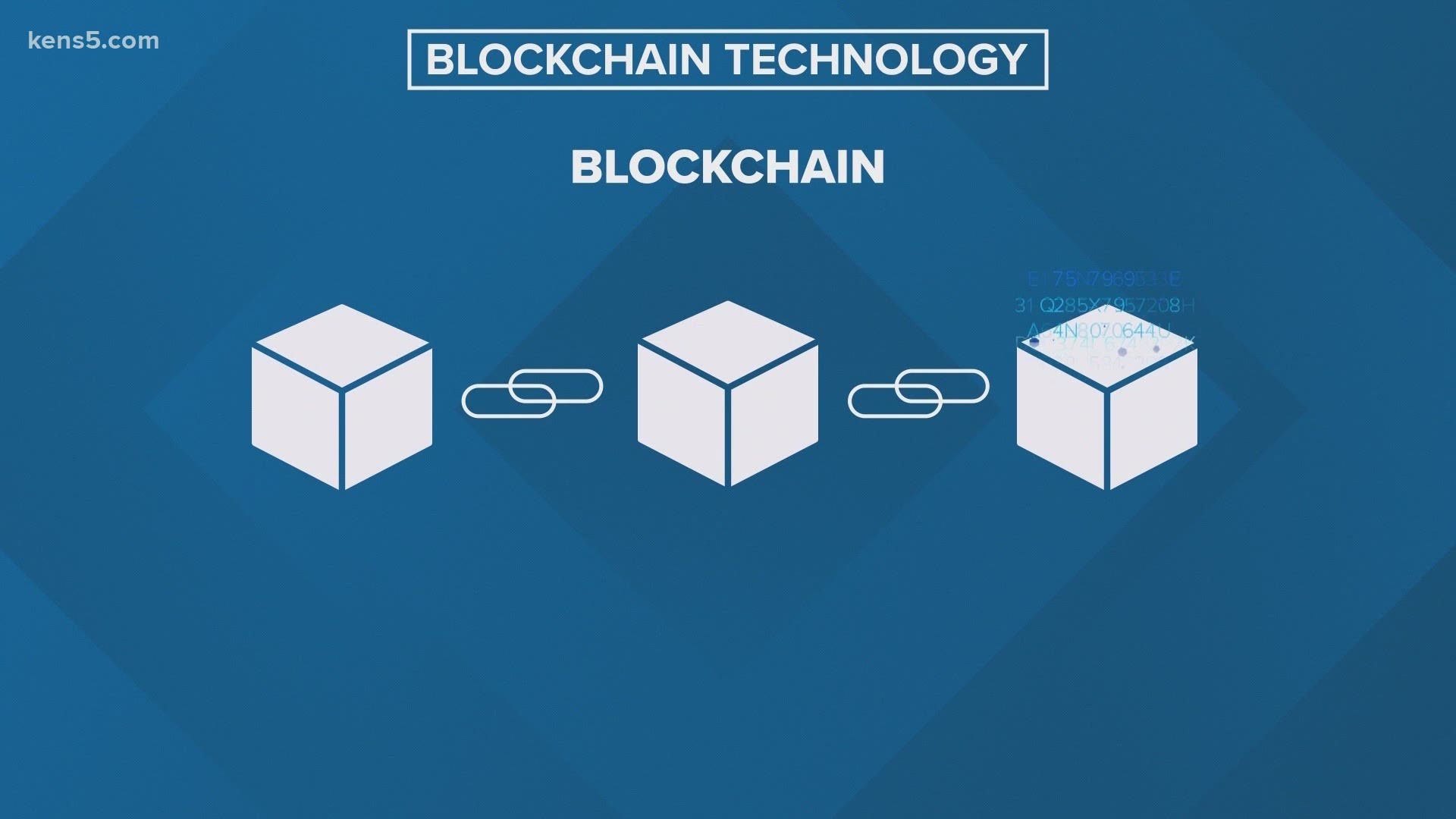

Like its name says, blockchain is information that’s chained together like blocks. Once new data is entered into the system, it’s timestamped and connected to all of the previous transactions, data or “blocks” before it.

Blockchain enthusiasts say this technology will revolutionize businesses. A real-life way to apply this technology is to streamline financial transactions with banks or contracts.

“One thing that would be great is if we can make the closing process, when we purchase a home or refinance a home, a little bit easier. We send all these documents to the lender and they require all these things,” Eggerss said. “Can blockchain be used for something like that?”

While it remains to be seen how blockchain technology could change lives on a large scale, the possibilities are far-reaching.

“These technologies may be confusing to many of us, I think we need to embrace it and say what are the possibilities and know that these things can evolve over time. The idea is that things can actually be more efficient,” Eggerss said.